Private credit’s third act: reconnecting support commodities

Understanding how market maturity is reshaping private risk credit

Private credit has moved from the edge of finance to an established component of the below-investment-grade credit markets. What began in the mid‑2000s as a relatively small and specialised form of nonbank lending has grown into a significant source of financing for small and medium‑sized companies, operating alongside the leveraged loan and high‑yield bond markets.

Growth has been substantial. Over roughly 20 years, private credit assets have increased nearly 20‑fold, reflecting both sustained investor demand for higher-yielding credit assets and changes in bank regulation. Today, private credit features prominently in corporate capital structures, institutional portfolios, and increasingly in banks’ own lending exposures through financing provided to private credit managers.

Recent credit events have brought greater attention to how risk is evolving as the market matures. Restructurings and write‑downs at borrowers such as Tricolor and First Brands, warnings about market stresses in late 2025, and more recent pressure linked to revised assumptions in certain software‑as‑a‑service (SaaS) business models underscore that private credit is subject to the same underlying economic forces that affect other risky credit markets.

Private credit’s third phase of development

The modern private credit market has evolved through three broad phases. The first phase followed the global financial crisis. Private credit managers expanded their role as direct lenders when regulatory changes and balance‑sheet constraints prompted banks to reduce small- and middle‑market lending. The second phase unfolded during the prolonged post‑crisis expansion. Low interest rates drove demand for yield, while borrowers favored private credit for its speed and execution certainty.

By mid‑2025, global direct‑lending assets had reached roughly $979 billion, up from about $148 billion a decade earlier, according to the alternative assets data provider Preqin. The broader private credit market totaled around $1.8 trillion, including more than $500 billion of committed but undeployed capital.

Today’s third phase reflects a more mature market structure. Its defining features are institutionalisation, increased interconnectedness with banks, and the influence of large amounts of available capital on competitive dynamics and underwriting standards.

Private credit is now embedded in portfolio construction decisions. Banks have become increasingly involved, not as originators of middle‑market loans but as providers of financing to private credit managers. Ample dry powder provides flexibility but also affects pricing, structures, and documentation, particularly later in the credit cycle.

How to think about private credit: Start with “credit”

Despite its bespoke structures and lesser transparency, private credit is fundamentally a form of credit exposure. Factors that influence leveraged loan and high‑yield bond outcomes—economic growth, financing conditions, and equity market performance—also influence private credit performance. The business cycle remains the primary driver of outcomes, though with less frequent price signaling.

Two implications follow. First, private credit behaves like risky credit, not as a substitute for it. While loans are often senior secured and floating rate, borrowers tend to sit at the lower end of the credit-quality spectrum. Second, outcomes depend on managers. Underwriting quality, portfolio construction, and restructuring capabilities can lead to meaningful dispersion across managers.

Are borrowers stretching to preserve liquidity?

Looking forward: Where risk may surface

As the market matures, risk is more likely to appear gradually than through abrupt dislocations.

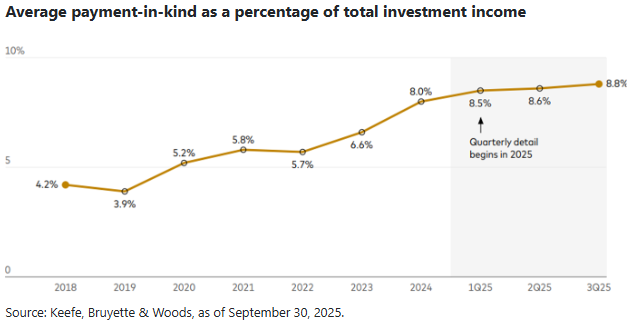

One such indicator is the use of payment‑in‑kind (PIK) interest, which allows borrowers to defer interest by adding it to principal. Intentional when included at origination, added later it can signify that cash is tight. In the direct‑lending market, PIK income averaged about 4.2% pre‑pandemic, rose to 7.4% post‑pandemic, and reached roughly 8.8% in the third quarter of 2025. Persistent increases have historically coincided with borrowers seeking to conserve cash. PIK also matters for public business development companies, which must distribute most taxable income even when that income is non‑cash.

Another area to monitor is underwriting discipline in an environment of substantial dry powder. Competitive pressures may show up first in greater leverage, looser covenants, more aggressive adjustments to earnings before interest, taxes, depreciation, and amortisation (EBITDA), and broader flexibility provisions—rather than in near‑term default rates.

Recent stress in software‑focused lending illustrates the point. As growth expectations for some SaaS models have been reassessed, loans underwritten on more optimistic assumptions have faced pressure. The broader point is that underwriting assumptions become most consequential when operating conditions change.

The important signals of competition and bank linkages

Private credit’s early growth shifted middle‑market lending away from banks, supporting financial stability by moving risk to fund structures better suited to this activity. Over time, banks have reengaged by financing private credit managers through vehicles such as subscription lines and net-asset-value facilities, which generally offer senior positioning, strong recoveries, and favorable capital charges.

From a systemic perspective, the primary consideration is less the likelihood of widespread private‑credit defaults and more the interaction between private credit liquidity needs and bank balance sheets. In a stressed environment, private credit vehicles may draw on bank facilities at the same time banks are tightening credit elsewhere.

As the market continues to mature, attention is shifting from growth to structure, underwriting discipline, and interconnectedness with the broader financial system. The performance of private credit going forward will depend less on its novelty and more on how it behaves across the credit cycle, particularly as competitive pressures and bank linkages increase.

Notes:

All investing is subject to risk, including the possible loss of the money you invest.

Diversification does not ensure a profit or protect against a loss.

Bond funds are subject to the risk that an issuer will fail to make payments on time, and that bond prices will decline because of rising interest rates or negative perceptions of an issuer’s ability to make payments.

Investments in stocks and bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966). The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance.

We have not taken your or your clients' objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard's financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice - Offer not to persons outside Australia.

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2026 Vanguard Investments Australia Ltd. All rights reserved.