Higher geopolitical risk premiums support commodities

Commodities delivered strong headline returns in 2025. Yet, beneath the surface, this rally was quite uneven—precious metals rose by roughly 80%, while the remainder of the Bloomberg Commodity Index underperformed cash by more than 3%.

Less than three months into the new year, the commodities rally may be broadening beyond precious metals to energy and non-precious metals. It’s early, but given that commodities are known for supercycles—those that can last over a decade, driven by long-term trends—it's worth considering what may be behind this broadening. The oil futures curve offers clues.

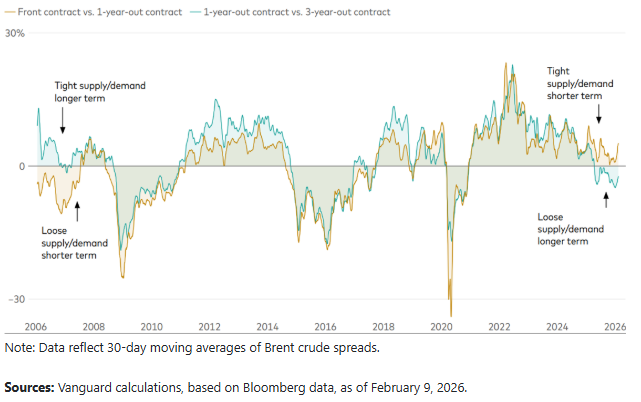

The accompanying chart shows two futures spreads over the last two decades. One line measures the price difference, or spread, between the near‑expiration Brent crude oil futures contract and the contract one year out. When the spread is positive, with near-term prices exceeding further-out prices, it typically signals near‑term excess demand or equivalent tightness in supply. A second line compares futures prices further out—the one‑year contract versus the three‑year—and captures longer‑term supply‑demand imbalances.

Expectations for oil supply and demand diverge over the short and long term

For much of the past two decades, these short- and long-term spreads have moved together, reflecting broadly consistent market views across time horizons. A notable exception occurred during 2006–07, toward the end of the last commodity supercycle, when strong long-term demand expectations—driven largely by China—supported longer-dated prices even as near-term fundamentals appeared less tight.

Another unusual exception—a reversal of the 2006–07 pattern—accompanies today’s broadening of the rally: Shorter‑term spreads indicate tight market conditions here and now, while longer‑term spreads suggest a lack of concerns about supply beyond a year out.

So, what’s behind the near-term tightness? Some of it may stem from a desire to build stockpiles, hedging against the potential for supply chain disruptions amid elevated geopolitical risks. At a deeper level, the evolving nature of globalisation, toward more fragmentation, may be at play. Nations’ efforts to prioritise resource security, reshore supply chains, and reduce strategic dependencies have the potential to reshape commodities markets. The resulting heightened competition suggests the possibility of higher risk premiums being priced into commodities, likely pushing up prices in the near term even as longer-term supply expectations remain comparatively well anchored.

Whether this condition lasts bears watching. If it remains a force over the coming years, commodities markets—particularly in critical minerals, gold, and energy—could command more persistent risk premiums than in prior decades.

Notes:

All investing is subject to risk, including the possible loss of the money you invest.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.